What To Know

- Thailand is facing a growing household debt challenge, with new data revealing a sharp rise in the number of people carrying financial burdens as the cost of living continues to climb.

- In contrast, younger individuals, particularly those aged 20–29, are increasingly turning to online lending platforms and installment-based purchases, with over a quarter in this group relying on such methods.

Bangkok Business News: Thailand Debt Surge Deepens as Costs Bite Harder

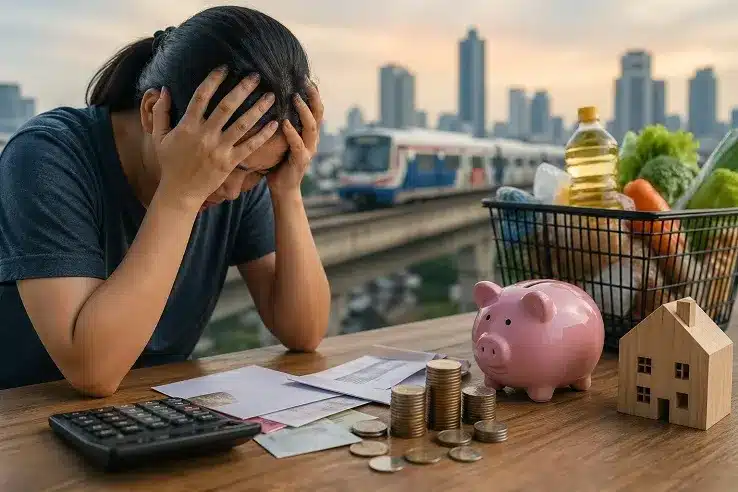

Thailand is facing a growing household debt challenge, with new data revealing a sharp rise in the number of people carrying financial burdens as the cost of living continues to climb. A nationwide survey conducted in February 2026 paints a concerning picture of economic pressure spreading across income groups, occupations, and age brackets.

Image Credit: Bangkok Business News

According to Nantapong Chiralerspong, director-general of the Trade Policy and Strategy Office, the survey gathered insights from 6,469 respondents and found that 62.44% of Thais are now in debt—up significantly from 50.99% just a year earlier. This Bangkok Business News report highlights a crucial turning point: rising daily living expenses have overtaken all other factors as the leading cause of debt, reflecting how inflationary pressures are reshaping household finances.

Rising Costs Drive Borrowing Trends

The data shows that nearly one-third of respondents, or 29.06%, attributed their debt to everyday expenses such as food, utilities, and transportation. Asset purchases—including homes and vehicles—followed closely at 25.83%, while borrowing for investment purposes accounted for 13.45%.

Lower-income households, particularly those earning below THB20,000 per month, were the most vulnerable to cost-driven debt. Many in this group reported borrowing simply to maintain basic living standards. Meanwhile, higher-income earners showed higher overall debt levels, often tied to asset acquisition or investment activities, indicating differing financial pressures across economic tiers.

Occupation and Age Reveal Uneven Burdens

Government employees, farmers, and self-employed workers were identified as the groups with the highest levels of debt. Formal borrowing—primarily from financial institutions—remains dominant, especially among older age groups. In contrast, younger individuals, particularly those aged 20–29, are increasingly turning to online lending platforms and installment-based purchases, with over a quarter in this group relying on such methods.

Students stood out with the highest proportion of online borrowing, reflecting both accessibility and potential risk. Meanwhile, individuals aged over 40 leaned more heavily on traditional financial institutions, suggesting generational differences in financial behavior and risk exposure.

Debt Repayment Pressures and Coping Strategies

Most respondents reported manageable monthly repayments, with nearly 39% paying less than THB5,000 per month. However, the burden rises significantly with income, as higher earners tend to carry larger repayment obligations.

To cope, many households are tightening budgets by reducing non-essential spending and seeking additional income sources. Financial planning and expense control are becoming increasingly common strategies, particularly among younger individuals. Older respondents, on the other hand, are more likely to seek debt restructuring or professional financial advice.

Outlook for 2026 Shows Cautious Sentiment

Despite high debt levels, 61.84% of respondents indicated they do not plan to take on additional debt in 2026. Among those who do, the primary reason remains unavoidable expenses, followed by refinancing existing debt and long-term investments.

Certain groups remain at higher risk. Farmers and self-employed workers anticipate borrowing to manage income volatility, while business owners are more focused on sustaining operations rather than expansion. Lower-income earners, especially those below THB10,000, face ongoing uncertainty, often driven by unstable income streams.

Economic Implications and Policy Response

The findings underscore a broader concern: household debt is not just a personal financial issue but a structural challenge affecting Thailand’s economic momentum. High debt levels can constrain consumer spending, reduce investment capacity, and increase financial vulnerability across society.

Authorities are responding by monitoring price levels, promoting domestic consumption, and supporting businesses in generating stable income streams. Efforts to ease living costs and expand economic opportunities are seen as critical to alleviating pressure on households.

Thailand’s debt landscape is entering a more complex phase, where rising costs, shifting borrowing behaviors, and income disparities intersect. The situation calls for careful policy management and increased financial awareness among the public. Without meaningful intervention, the risk is not just higher debt, but a deeper strain on economic resilience and long-term growth prospects.

For the latest on the Thai economy, keep on logging to Bangkok Business News.