What To Know

- The latest data paints a worrying picture of an economy where many households are struggling to keep pace with rising living costs and uneven income recovery.

- The increase is being supported by lending from state-owned financial institutions and specialized lenders, as well as a sharp rise in borrowing from savings cooperatives and pawnshops.

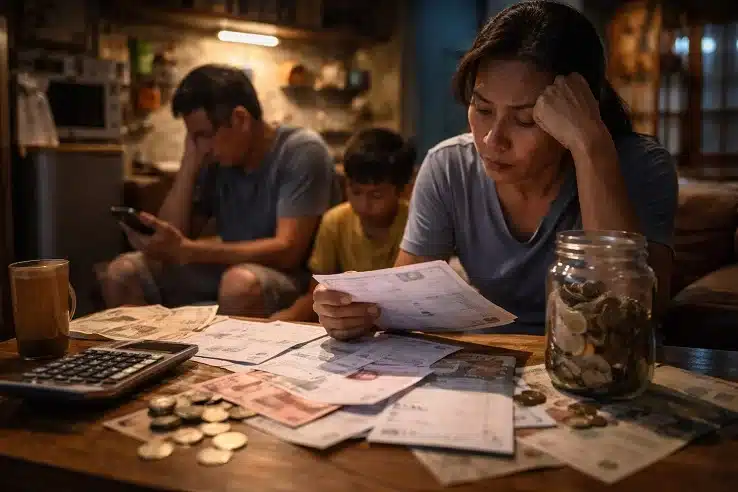

Bangkok Business News: Thailand’s household debt has surged to 86.7% of gross domestic product, reflecting a growing dependence on borrowing not for investment or asset building, but for everyday survival. The latest data paints a worrying picture of an economy where many households are struggling to keep pace with rising living costs and uneven income recovery.

Image Credit: Bangkok Business News

Borrowing Shifts Toward Daily Survival

Thailand’s total household debt climbed to 12.72 trillion baht in the fourth quarter of 2025, rising by about 119 billion baht from the previous quarter. This Bangkok Business News report highlights that the increase is being driven primarily by personal consumption loans, indicating that households are increasingly relying on credit to cover basic daily expenses.

This shift marks a significant change in borrowing patterns. In previous years, loans were more closely tied to long-term investments such as housing or business expansion. Now, borrowing is being used simply to maintain daily living standards. Housing loans have grown only marginally, while other types of credit including hire-purchase loans for vehicles, education loans, and business loans have continued to decline.

Traditional Lending Tightens as Informal Credit Expands

A closer look at lending trends reveals a tightening of credit conditions among private financial institutions. Commercial banks and other major lenders have become more cautious, leading to a contraction in formal lending channels.

Outstanding loans from commercial banks have fallen by around 2% year-on-year, marking the seventh consecutive quarter of decline. Credit card lending, leasing, and personal loans have also continued to shrink, extending a downward trend that has persisted for several quarters.

Despite this, overall household debt continues to rise. The increase is being supported by lending from state-owned financial institutions and specialized lenders, as well as a sharp rise in borrowing from savings cooperatives and pawnshops. These sources offer easier access to credit, particularly for individuals who may no longer qualify for traditional loans.

This shift toward more accessible but potentially riskier forms of borrowing suggests that many households are facing liquidity pressures and turning to short-term solutions to stay afloat.

Labor Market Weakness Deepens Financial Strain

The growing reliance on credit is closely linked to ongoing weaknesses in the labor market. Thailand’s unemployment rate rose to 0.9% in the early months of 2026, with young job seekers facing increasing difficulty entering the workforce.

Employment among those aged 15 to 24 has declined for a second consecutive year, reflecting limited job opportunities and weaker demand for new entrants. Many young workers have been pushed into informal employment, where income tends to be lower and less stable.

The industrial sector has also shown signs of contraction, marking its first decline in four years. This aligns with broader economic softness and ongoing challenges in the manufacturing sector. While some workers have transitioned into the service sector, this segment has limited capacity to absorb additional labor, and many jobs offer relatively low wages.

At the same time, new business registrations have declined, indicating weaker private investment and fewer opportunities for job creation.

Rising Living Costs Add Further Pressure

External factors are adding to domestic challenges. Rising geopolitical tensions have pushed up global energy prices, increasing the cost of living and placing additional pressure on household budgets.

Inflation is expected to accelerate to around 3.2% in 2026, eroding real wages that have only recently recovered to near pre-pandemic levels. Higher energy costs are also raising business expenses, which could limit wage growth and hiring in the near future.

Several sectors, including agriculture, construction-related industries, and petrochemicals, are particularly vulnerable to rising input and transportation costs. At the same time, exports to affected regions have slowed, placing further strain on industries that employ millions of workers.

As businesses attempt to manage rising costs, workers may face reduced hours, lower overtime pay, or slower wage increases, further weakening household income.

Policy Measures and Long-Term Outlook

In the near term, targeted government measures aimed at reducing living costs, particularly energy expenses, could help ease the burden on vulnerable households. Temporary and well-focused support could strengthen purchasing power and reduce the need for additional borrowing.

Efforts to restructure existing debt will also be critical in helping households manage their financial obligations and improve liquidity during a period of slow income recovery.

Over the longer term, addressing the root causes of high household debt will require a broader strategy focused on increasing income levels and improving earning potential. This includes investing in workforce skills, promoting higher-productivity industries, and expanding access to better-paying job opportunities.

Strengthening social welfare systems and encouraging financial discipline will also be key to building long-term resilience and reducing reliance on consumption-driven borrowing.

Thailand’s rising household debt is not just a financial concern but a reflection of deeper structural challenges within the economy. The increasing use of credit for everyday expenses highlights the pressure faced by households navigating a fragile labor market and rising living costs. Without sustained and effective policy intervention, the risk of worsening debt burdens and reduced repayment capacity could continue to grow. Addressing these challenges will be essential to restoring financial stability and ensuring more sustainable economic growth in the years ahead.

For the latest on the Thai economy, keep on logging to Bangkok Business News.